1.0 Introduction

We assess that Ukraine’s drone economy is viable under fire, conditionally sustainable beyond it, and exportable in ways that are deepening fast. At the same time, we find that it is vulnerable to a ceasefire, to Chinese supply chain interference, and to institutional fragility.

Three questions organize what follows: is the system viable, is it sustainable, and is it exportable? Each section addresses a dimension of the ecosystem through these lenses. The evidence supports one overarching judgment: Ukraine’s drone economy is a knowledge network for which most irreplaceable assets are already migrating beyond Ukraine’s borders. Its ultimate value will be determined by how much of that migration is completed before the outcome of the war arrives, not by the outcome itself.

2.0 Drone Economy: System Character

Ukraine’s drone economy moves between decentralized agility and centralizing correction. That oscillation defines the system’s character. The industry grew from less than ten manufacturers in 2022 to over 500 by 2026. Three structural features explain the system’s behavior: the performance-linked procurement loop; the corruption problem rooted in the wartime opacity the system needs to function; and the financial support which holds it all up. Defense Minister Fedorov’s digital reforms are the most serious attempt yet to stabilize these tensions.

2.1 Supportive Evidence

Ukraine’s drone economy did not emerge from a pre-existing industrial strategy. It grew from fewer than ten domestic manufacturers in February 2022 to over 500 by 2026, producing roughly 2.2 million unmanned systems in 2024 and tracking toward 4.5 million in 2025. This is likely more than the combined output of all NATO members. The scale matters first: this is a functioning industry moving faster than any Western procurement system has matched.

[source, source, source, source]

2.1.1 Drone Economy Character: Asymmetric Oscillation

Kyiv keeps trying to centralize a system that works best decentralized. However, each attempt makes things worse before it corrects.

The December 2024 certification regulations are the clearest case. They extended delivery times and opened new paths to corruption instead of standardizing. Contracts grew dependent on paperwork that could be manipulated. Front-line supply degraded. The Ministry’s response was to give $60 million in monthly direct brigade funding from January 2025, with Minister Umerov instructing commanders to buy what fits their mission. This was a decentralizing fix to a centralizing mistake. This pattern repeats throughout the war.

2.1.2 Drone Economy Character: Adaptivity Mechanism

The system’s adaptivity is not cultural. It is built into infrastructure. The Army of Drones Bonus program generated 819,737 video-confirmed strikes in 2025 alone. This includes nearly 240,000 personnel eliminations, 62,000 vehicle hits, 32,000 enemy UAV strikes, per Ukrainian MoD data. Fedorov has called this the first time Ukraine has had “real, verified battlefield data” to drive management decisions.

DOT-Chain and the Army+ platform close the loop from the manufacturer side: malfunction and performance data route directly to manufacturer dashboards in real time, cutting design iteration from months to weeks. By April 2026, 95% of drone units used the e-Points system, which delivered over 181,000 systems worth USD 310 million that year alone.

[source, source, source, source, source]

2.1.3 Drone Economy Character: Structural Corruption

Corruption here is the predictable cost of the opacity that wartime speed requires. In August 2025, National Anti-Corruption Bureau of Ukraine (NABU) and Specialized Anti-Corruption Prosecution Office (SAPO) uncovered a major graft scheme in drone and EW procurement. This included kickbacks up to 30% of contract value, implicating a sitting Rada lawmaker, local officials, and National Guard personnel. A separate investigation examined alleged cost inflation by manufacturer Fire Point, with reported ties to figures close to Zelensky.

These cases are not isolated. Political and business interests with direct stakes in contract flow have long shaped Ukraine’s defense industrial base. These are interests that survived 2022 by adapting to the new procurement environment. NABU’s findings point to structured rent-seeking by actors with institutional access, not random opportunism. Fedorov’s response of firing five deputy ministers on taking office, launching an industrial audit, mandating automated procurement, is the most aggressive yet attempted.

[source, source, source, source]

2.1.4 Drone Economy Character: Emergent Exportability

Ukraine opened formal arms exports on 27 April 2026. The Drone Deal framework sells a system, not a product: ten-year agreements with Saudi Arabia, the UAE, and Qatar bundle drones, air defense, electronic warfare, pilot training, and doctrine together. Export offices have opened in Berlin and Copenhagen. Under the Build with Ukraine initiative, launched at Ramstein in June 2025, Ukraine is building production lines in Slovakia, Finland, and Denmark, with engineers already training partner air defense units abroad.

The choice is to monetize the knowledge system instead of the hardware. LSE IDEAS’ 2025 research backs this up. The human capital in Ukraine’s drone ecosystem is a scarce asset, and no hardware purchase can replicate it.

[source, source, source, source, source]

2.1.5 Drone Economy Character: Sustainable Sustainability

Ukraine’s drone economy cannot finance itself. The Ramstein Contact Group and the Danish model are load-bearing.

The Danish model channeled USD 6 billion to Ukrainian production in 2025, on top of a USD10 billion domestic MoD budget. This represents a 60% expansion of purchasing power beyond what Ukraine could fund alone. Eight capability coalitions, including a Drone Coalition co-led by Latvia and the UK, now run on roadmaps through 2027. Germany pledged USD 12 billion for 2026 with a UAV and air defense focus; Sweden committed USD 2.6 billion annually; the Netherlands directed USD ~ 450 million straight to Ukrainian-made drones.

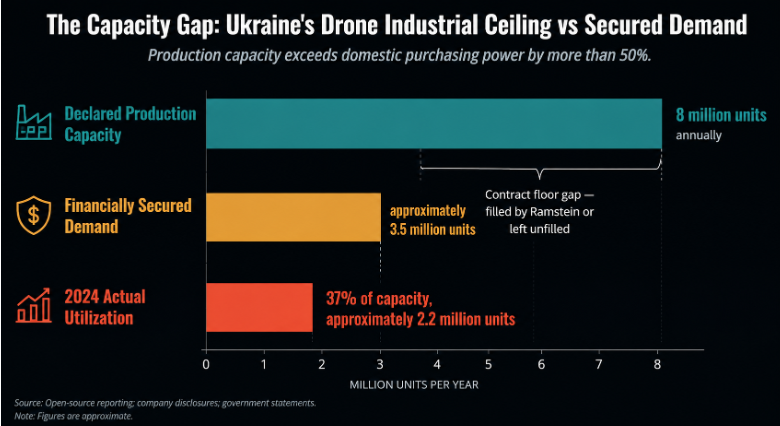

The February 2026 Ramstein meeting, under Fedorov, secured a record USD 38 billion pledge for the year, with tighter oversight. This hedges near-term risk. But the production ceiling still exceeds domestic purchasing power by a wide margin: Ukrainian manufacturers ran at just 37% capacity in 2024 despite record budget allocations.

[source, source, source, source, source]

2.2 Mechanism

The Ukrainian drone economy’s behavior is produced by three mechanisms. The first is Ukraine’s Army of Drones Bonus system. This converts video-confirmed battlefield results into purchasing credits, redeemable through the Brave1 Market. In turn it creates a direct transaction process from the front line to the factory. Manufacturers whose systems perform get more orders and those whose systems fail get less. The DOT-Chain Defence platform and Army+ application digitize the feedback half of the loop. This compresses the process from months or years to just days or weeks. This mechanism is what produces the system’s adaptivity.

The second mechanism is that the Ukrainian state is the only buyer of Ukrainian drones at scale. But Ukraine adapted this exclusivity to enforce competition. Brave1 Market lists over 4,000 products from competing manufacturers. Direct brigade procurement gives front-line commanders purchasing discretion. The e-Points performance data makes supplier quality visible across the system. The result is a combination of the state’s purchasing power with genuine competitive pressure on producers. However, any disruption to state contracts immediately affects the whole system.

The third mechanism is the Danish model. This channels partner-country funds directly to Ukrainian manufacturers. It insulates production from domestic budget volatility and protects the demand side beyond what Ukraine could sustain alone. However, because of this, the production base has scaled to a capacity level that requires this external demand to survive.

[source, source, source, source, source]

2.3 Implications

Viability for Ukraine’s drone economy is established for the duration of active conflict. Sustainability is currently upkept by European partners through the Ramstein mechanism. The critical variable is not present commitment but post-conflict political will. Exportability has moved from theoretical to operational, but its strategic significance lies in that Ukraine is attempting to export the mechanism, not just the product.

2.4 The Source of Risk

In our estimation, four structural risks demand immediate attention.

The first risk is instability at the top. Fedorov’s reforms are the right medicine, but they are built around one person’s mandate. Ukraine has changed defense ministers repeatedly since 2022. What Fedorov is building has not yet survived a single leadership transition. If he goes, the reform agenda may go with him. Fedorov now holds authority over Brave1, the digital procurement architecture, the e-Points system, Mission Control, and the MoD itself. This means that the system’s current trajectory is dependent on Fedorov.

The second risk is the contract floor problem. Manufacturers are operating well below capacity because contract flow is inconsistent. Companies making battlefield technology are sizing their workforce and investment based on demand signals that can disappear with a budget revision or a shift in European political mood. Without longer-term procurement commitments, the production base will not be able to scale.

The third risk is corruption as a credibility problem. The August 2025 scandal is not just a domestic problem. It follows Ukraine into every export negotiation and every co-production discussion. Fedorov has tackled the problem. The Drone Deal framework carries reputational risk that partners will factor in future calculations.

The ceasefire trap is the fourth risk. Everything that makes this ecosystem exceptional such as existential national pressure, live battlefield feedback, and Western financing, all disappear when the war stops. Ukraine has no tested model for what the industry looks like when that happens.

3.0 Economic Drivers

Ukraine built this industry larger than battlefield necessity required. That gap between what the war demanded and what Kyiv chose to build is the subject of this section. Three drivers explain it.

The clearest proof that the strategy is already operational. In March 2026, Ukraine deployed specialist counterdrone teams to five Middle Eastern countries (UAE, Saudi Arabia, Qatar, Kuwait, and Jordan) to protect against Iranian Shahed drone attacks. As of that deployment, Ukraine had 201 military experts operating across the Gulf region, with 34 more prepared to deploy. Ukraine sent this while fighting its own existential war demonstrating high capability, and reliability.

3.1 Mapping Drivers and Strategic Logic

The first driver behind this drone ecosystem is existential signaling. Ukraine has consciously used the scale and sophistication of its drone industry to argue that it is a productive partner. The 2025 Defense Tech Valley summit which hosted 5,000 participants from 50 countries, and featured $100 million in signed memoranda was a diplomatic instrument to that end. Zelenskyy’s decision to open managed arms exports exclusively to countries Ukraine “can count on” shows that Ukraine’s drone industry is a selective partnership mechanism.

The second driver is post-war economic positioning. The ambition to become Europe’s defense technology hub predates any realistic export market and exceeds what the war requires. Brave1 investment disclosures show that investment rose from USD 1.1 million in 2023 to over USD 105 million in 2025. Ten Ukrainian defense export centers have been established across Europe. The behavior is consistent and shows that Ukraine is aiming to be a hub of defense production.

The third driver is the system’s export irreversibility as a security strategy. Kyiv has pursued deep integration into European defense architecture to make its own survival a vital European interest. The EU White Paper for European Defence Readiness 2030 names Ukraine as the frontline of European security and mandates integration of Ukrainian industry into the European Defence Technological and Industrial Base. The European Commission has secured drone procurement within its support facility through 2027. Carnegie Endowment analysis asserts that creating robust industrial cooperation now serves European strategic interests regardless of ceasefire outcome in Ukraine. Therefore, this driver has largely driven deep successes into EU-Ukrainian relations.

[source, source, source, source, source]

3.2 Tensions and Risks

The primary risk specific to behind all three of these drivers is intellectual property. The same partnerships that embed Ukraine in European and American defense architecture also expose its most valuable asset which is battlefield innovation, to transfer without adequate protection. The Atlantic Council has flagged that without robust IP legislation and explicit ownership protections in every licensing and co-production agreement, Ukraine could secure its survival on the battlefield while losing the innovation economy that should underpin its recovery. A co-production deal structured poorly is a knowledge extraction mechanism disguised as partnership.

[source]

4.0 Structure of the System

Ukraine’s drone industrial base is a three-tier production pyramid running on five funding channels, held together by a digitally institutionalized feedback loop, and dependent on Chinese components its own government is racing to replace. This section maps those components to locate where the structural vulnerabilities actually are.

4.1 Sketching out the System

4.1.1 Tiers of Production

Ukraine’s production base grew from fewer than ten manufacturers before the invasion to over 500 by 2025.

Tier 1 holds the institutional weight. TAF Drones scaled from 6,000 to 40,000 units in 2024, generating USD160 million in first-half revenue, and distributes production across multiple cities to resist Russian strikes. UkrSpecSystems operates facilities in the United Kingdom. Fire Point localized 97.5% of engine components, cutting silencer costs from USD 450 to USD 80 per unit, and produces over 200 long-range strike drones daily. These firms have international footprints, direct state contracts, and fallback revenue when domestic demand drops.

Tier 2 are bootstrapped mid-scale manufacturers built on state contracts and founder capital. They drive most product innovation. The largest took two to three years to scale and are now opening factories in Germany and Denmark. This tier is the most contract-exposed. It is also where the next generation of systems is being designed.

Tier 3, the cottage and volunteer assembly base, contributed substantially to Ukraine’s 1.5 million FPV output in 2024. Individually replaceable. Losing it cuts volume, but not capability.

[source, source, source, source]

4.1.2 The Military Factor

The USF comprises 2% of Ukraine’s armed forces and accounts for 35% of confirmed enemy destruction. Under commander Robert “Madyar” Brovdi, appointed June 2025, it unified its core brigades with the Drone Line’s five elite strike units (the 414th Magyar’s Birds, 20th K-2, 412th Nemesis, 427th Rarog, and 429th Achilles) spanning operations from front-line FPV to deep strikes 2,000km into Russian territory.

The USF does not command all Ukrainian drones. The Navy, Marine Corps, Air Force, and most ground brigades run independent units. The USF maintains contact with most domestic manufacturers, tests systems, routes feedback to developers, and has integrated over 170 unmanned systems. The same distributed architecture that makes the system resilient makes it hard to standardize.

[source, source, source, source, source, source]

4.1.3 The Resources of the Drone Economy

Five channels sustain the production base.

The state MoD budget covered 96% of drone needs in 2024 per Umerov’s figures, but domestic purchasing power still falls well short of total production capacity. Brave1’s 2025 grant budget of USD 75 million funds early-stage development and component localization across 240 grants. Private and venture investment scaled from USD 5 million in 2023 to USD 105 million in 2025. Ukraine now attracts the majority of European early-stage defense tech investment at seed and Series A. The Ramstein-Danish model adds USD 6 billion in structured procurement. Oschadbank has issued USD 837 million in bank guarantees to four UAV manufacturers under the Netherlands framework, enabling manufacturers to begin production before contracts clear.

Three of five channels (Ramstein, private foreign investment, and partner guarantees) depend on Western political and commercial confidence that is present but not guaranteed.

[source, source, source, source, source, source, source, source, source]

4.1.4 The Supply Chain and China

In 2022, Ukraine imported 99% of finished drone systems. By 2025, it imports 99% of components predominantly from China. The direction has reversed. But the destination has not been reached.

F-Drones illustrate the pace. Entirely Chinese-sourced in 2023, they produced flight controllers, speed regulators, radio modems, and video transmission systems domestically by 2025. Zelenskyy confirmed in April 2025 that 11 Ukrainian enterprises mastered fiber-optic drone production, with over 20 certified fiber-optic models appearing in early 2025 alone.

China’s response: manipulate component pricing to make finished imports cheaper than the raw materials Ukraine needs for true independence, and tighten export controls on those raw materials. Brave1 launched a dedicated localization initiative at the end of 2025. The race between Ukraine’s verticalization timeline and China’s interference is active and unresolved.

4.1.5 The Drone Economy’s Capabilities

The system’s limits are structural. Domestic purchasing power covers 37–50% of production capacity. Quality standardization across 500+ producers remains unsolved — three certification attempts since 2022 each generated corruption and bottleneck problems of their own. Swarm operations are capped at groups of 3–25 drones across roughly 100 test operations. Western cloud infrastructure dependency persists; edge computing is only a partial answer.

[source, source, source, source, source, source, source, source, source]

4.2 Mechanisms

Three mechanisms drive the system.

The first is tiered production under competitive pressure. The state buys at scale but does not dictate production methods. Tier 1 holds contracts and relationships, tier 2 holds innovation. Lastly, tier 3 holds volume. All three compete for the same procurement pool through Brave1 Market and direct brigade contracts — performance determines market share. The structural weakness: one contract shock hits all three tiers simultaneously.

The second is the feedback compression loop. DOT-Chain and Army+ route front-line performance data directly to manufacturer dashboards in real time. Commanders buy what works and stop buying what does not. Poor-rated manufacturers lose orders in weeks, not procurement cycles. Design iteration compresses from months to days.

The third is external demand buffering. The Ramstein-Danish model adds USD 6 billion in structured procurement above Ukraine’s MoD budget. Without it, manufacturers operate below 40% capacity. With it, the production base sustains workforce and investment decisions beyond the immediate contract horizon. The same channel that provides stability also transmits European political risk directly to Ukrainian factory floors.

Under stress, these mechanisms compound each other’s failures. A budget shock cuts state contracts, starves Tier 2, slows the feedback loop, and is only partially offset by Ramstein financing.

4.3 Implications and Risk

Viability holds as long as the tier structure functions. However, the real risk is hollowing of the middle. A sustained procurement gap does not threaten Tier 1, which has international revenue to absorb the shock. It quietly starves Tier 2, where the next generation of systems is being built. The supply chain risk is more immediate. Ukraine depends on Chinese components for systems fighting a war China’s strategic partner is prosecuting. Beijing has not weaponized this yet. The pricing manipulation already underway demonstrates it can. A targeted export restriction under battlefield pressure would produce a critical supply shock. Brave1’s localization program is the right response. It is not yet sufficient. The gap between Ukraine’s verticalization timeline and China’s interference capacity is the most underappreciated vulnerability in the ecosystem.

Exportability is structurally fragile. The Drone Deal sells training, doctrine, and co-production. These all require Tier 1 and Tier 2 firms to deploy engineers abroad while supplying the front line simultaneously. That works in a surplus environment but breaks under escalation. Any significant uptick in combat activates the military priority clause in every export agreement, suspending the deliverables that make the export offer credible in the first place.

5.0 Ukraine and the Rest: Global Competition

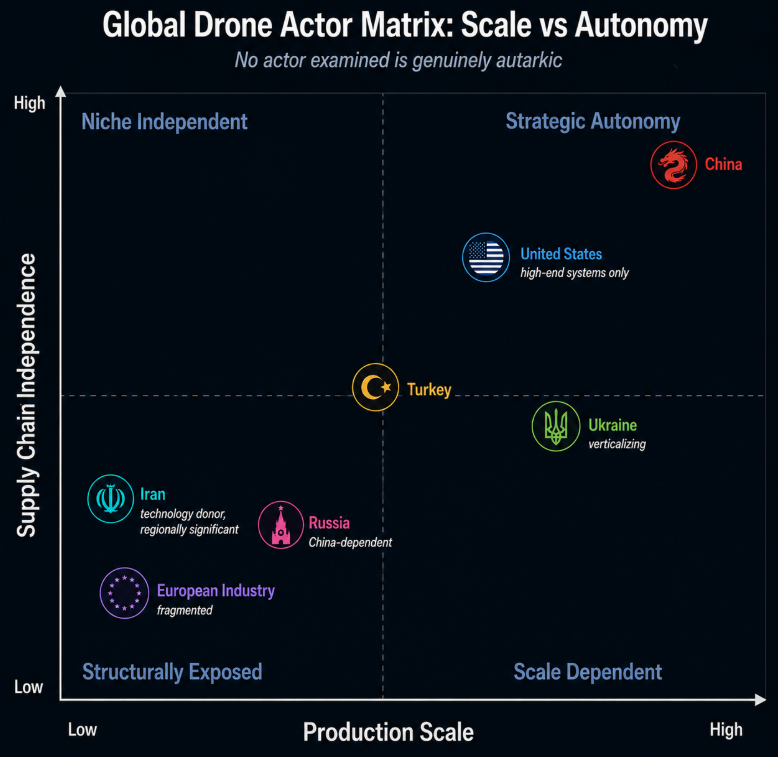

5.1 China: The Supply Chain Holder

China is not competing with Ukraine’s drone economy but is its foundation. China controls an estimated 80% of the global drone component supply chain. China’s strategic posture in the drone domain is not primarily about battlefield performance but about standard-setting, supply chain leverage, and export volume. Chinese firms are exporting products, systems and standards. In turn, they shape international operational benchmarks across the economy.

This makes China more than just a competitor. Beijing does not care to beat Ukraine on the battlefield. Ukraine is China’s most consequential drone customer and its most dangerous proof of concept at the same time.

5.2 Russia: The Illusion of Autarky

Russia’s drone program is the clearest case study available for what industrial scaling under sanctions looks like. Alabuga is now producing over 5,500 Shahed-type drones per month, hitting its 6,000-unit contract target a year ahead of schedule. Unit costs are falling from USD 200,000 in 2022 to approximately USD 70,000 in 2025. However, the CEO’s public claim of complete autarky is directly contradicted by evidence. Investigators traced at least 41 critical components back to Chinese suppliers.

Russia has achieved impressive industrial scaling but not independence. Its drone program would degrade significantly within months of a genuine Chinese supply restriction. More analytically significant for this report is that Russia’s drone economy has no feedback loop comparable to Ukraine’s. Alabuga produces at volume for a predetermined design. Launching hundreds of drones nightly to exhaust Ukrainian air defenses is effective because it does not require adaptivity. It needs scale and cost where Russia is very competitive.

5.3 Iran: The Donor Hollowed out

Iran built the template Russia now operates and has been sidelined by its own creation. After transferring blueprints, software, and manufacturing knowledge to Moscow, Tehran finds itself marginal to a program it originated. Russia’s upgrades (improved communications, larger warheads, jet-powered Geran-3 variants) caught Iran off guard. A Western intelligence source described this as a gradual loss of control over the final product, now manufactured largely without Iranian input. Iran’s regional drone capability remains consequential. But globally, it is now a technology donor whose most important export was absorbed, upgraded, and partially surpassed by its recipient. Ukraine should study this carefully. Technology transfer at scale, without IP protection and commitment, produces a partner that eventually no longer needs you.

5.4 Turkey: The Closest Comparison

Turkey is the most instructive comparison for Ukraine’s export ambitions. Baykar hit USD 2.2 billion in exports in 2025 making it the world’s largest armed drone exporter for the third consecutive year. Its advantages are combat validation across multiple conflicts, unit costs well below Western equivalents, and no political conditions attached to sales. Turkey sells to buyers the US and EU will not supply.

But it is not autarkic. Electro-optical sensors, engines, and imaging systems still come from Canada, Germany, and Ukraine. Canadian export sanctions in 2020 disrupted production. The Turkey-Ukraine relationship is cooperative, not competitive. Baykar uses Ukrainian engines in its Akinci and Kizilelma platforms and is building a facility in Ukraine.

[source, source, source, source, source]

5.5 United States: The Student

The US leads in high-end military drone capability and lags badly on everything Ukraine has demonstrated at scale. The Pentagon’s updated drone strategy mirrors Ukrainian practice directly: delegating procurement to unit commanders, shortening development cycles, citing DOT-Chain by name. However, the gap between aspiration and delivery is large. Replicator delivered hundreds, not the thousands targeted by August 2025, with persistent technical failures and systems too expensive to procure at needed volume. The Army wants one million expendable drones by 2028. FY2027 budget requests exceed USD 70 billion for drones and counter-drone systems. The US is thus a potential customer, a co-investor, and a potential extractive partner if IP protections are not negotiated carefully.

5.6 European industry: The most important partner, the most fragmented actor

Europe is Ukraine’s most important strategic partner and its most structurally limited one. The EU invested USD 1.1 billion in 57 defense projects under the 2025 EDF. Ten Ukrainian production facilities are being established across Europe in 2026. EDIP earmarks about USD 300 million for a Ukraine Support Instrument with direct Brave1 funding. But Europe’s own drone industry is the problem. The Eurodrone program, conceived in 2014, now targets 2031 delivery. France withdrew in October 2025. The French Air Force chief called it “yesterday’s drone that we can get tomorrow.” Europe’s legacy procurement timelines are incompatible with Ukrainian iteration speed. The IP question also remains unresolved. Until that is settled, the co-production framework is a serious pilot, not a durable architecture.

[source, source, source, source, source, source]

5.7 The Autarky Question

No actor examined here is genuinely autarkic. Russia’s drones run on Chinese components. Turkey’s UAVs need Canadian sensors and Ukrainian engines. The US cannot replace Chinese components at scale without years of investment. Ukraine depends on Chinese electronics for systems fighting a war China’s strategic partner is prosecuting. European industry cannot match Ukrainian speed without Ukrainian knowledge. China’s dominance depends on global markets including those of its stated adversaries. The contest is over node control: who supplies what others depend on, who sets the standards others comply with, and who holds the operational knowledge no catalog can replace. On supply chain and standards, China leads. On operational knowledge, Ukraine leads by an order of magnitude no competitor can close without replicating the conditions that produced it.

6.0 Trajectory & Value: Where is the Ukrainian Drone Economy Going

This section looks at what the drone economy may become under three scenarios:

A) a continued high-intensity conflict,

B) a negotiated settlement, and

C) a Russian military victory.

Each examines the drone economy against the viability, sustainability, and exportability vectors. Across all three of these vectors it is evident that the Ukrainian drone economy has been structured so that its value does not reside exclusively within Ukraine’s borders.

6.1 Scenario A: Continued High-Intensity Conflict

Continued war is Ukraine’s drone economy’s best outcome and harshest test. The performance dimension is established. What is less examined is what sustained conflict does to the system’s structural integrity over time.

The production base is scaling faster than its institutional foundations can absorb. Ukraine has declared capacity for over 8 million annually which is a ceiling it cannot finance domestically without demand. The human capital dimension enhances this. Ukraine’s drone economy runs on a specific generation of engineers, operators, and procurement specialists. Sustained conflict consumes this generation faster than the educational process can replace it.

The exportability trajectory under continued conflict is the most consequential near-term output. During every month of active combat, co-production facilities in Germany, Denmark, and the Baltics are operational, Ukrainian engineers are embedded in European partner institutions, and IP agreements are being signed and tested in real-time. The knowledge base becomes less exclusively Ukrainian and more durably European.

The viability of the system under Scenario A is therefore not in question for the immediate term. The sustainability question is where the pressure accumulates because the production base may be scaling beyond its ceiling. At the same time its human capital is being consumed faster than is replaced.

6.2 Scenario B: Negotiated Settlement or Ceasefire

A negotiated settlement is the scenario for which Ukraine’s drone economy is the least prepared for and the most exposed to. The urgency that justifies financing and corruption goes away. What remains is an industrial base producing at a scale that peacetime Ukraine cannot finance. Without an active front line, the feedback mechanism loses its primary input. Manufacturers competing on battlefield performance metrics have no metric to compete on.

The sustainability exposure is severe. Ukrainian manufacturers were operating at 37% capacity in 2024 despite record budget allocations and an active war. A ceasefire removes both the domestic urgency that drives procurement and the Western political narrative that justifies Ramstein financing. The export framework is the system’s most credible peacetime lifeline. Its adequacy depends on whether export revenues can replace Ramstein financing and whether the military priority clause written into export agreements can be retired without triggering complications with partners.

6.3 Scenario C: Russian Military Victory

A Russian military victory would not destroy Ukraine’s drone economy. It would separate the tangible assets that can be captured from the intangible ones that cannot.

6.3.1 What Russia can take

The tangible assets of Ukraine’s drone economy are real and should not be underestimated. These include production equipment, tooling, component supply relationships, testing infrastructure, and physical manufacturing nodes. Fire Point’s production lines, TAF Drones’ distributed facilities, the component localization investments in motors, antennas, and carbon fiber fabrication are all capturable. Russia’s experience at Alabuga demonstrates that it can absorb foreign drone production blueprints and scale them under pressure.

6.3.2 What Russia can’t take

The ecosystem that makes that infrastructure productive is not something Russia can take. The engineers leave. The feedback loop dissolves without an active front line and without the link between operators, procurement staff and manufacturers. The DOT-Chain architecture, Mission Control, and the e-Points database can be moved. But the physical server infrastructure is vulnerable.

Russia’s strategic interest in a victory scenario therefore is elimination, not capture. A Russian-controlled Ukrainian drone industrial base, stripped of its human capital, would produce less at a fraction of current capacity. This is not a prize for the Kremlin but rather a liability.The systematic targeting of Ukrainian production facilities, drone schools, and defense-technology infrastructure reflects Russia’s strategic preference for destruction.

The European dimension of Scenario C is where our analysis becomes most significant. The co-production facilities established across six European countries, the Ukrainian engineers working with partners, the export network are all assets that do not revert to Russia in any way. They are already outside Ukraine’s borders and already generating institutional knowledge. A Russian victory accelerates this. Europe’s drone-industrial dividend in this scenario is real but incomplete. Europe wins a foundation of a defense-industrial capability but loses the battlefield.

Russia’s position as a global power is not meaningfully enhanced by capturing Ukraine’s drone industrial base. The physical assets without the ecosystem do not produce a capability Russia does not already possess through Alabuga and its Chinese supply chain. What a Russian victory does is it eliminates the most credible proof of concept for a non-Chinese, non-Russian drone industrial model built under peer-conflict conditions.

7.0 Conclusion

Ukraine’s drone economy is a functioning defense-industrial ecosystem for which the most valuable assets are operational knowledge, institutional architecture, and human capital. These assets are already being distributed across the West. Assessed against the three questions that have organized this report, the system is viable under pressure, conditionally sustainable beyond it, and exportable with continued integration across Western systems.

Russia’s strategic interest in Ukraine’s drone economy is to eliminate, not capture, it. On the other hand, European investment in Ukraine pays back in each scenario but with different types of benefits. The most fascinating lesson that the Ukrainian drone economy has to teach is taught by its warriors and those with experience in building it. In this sense, it is as exportable, viable and as sustainable abroad as its receivers are willing and able to absorb and integrate it.